By - Jeremiah Grant

Last Updated - December 24th, 2024 11:25 AM

Dec 24

Valuing a company at different stages of its development can provide valuable insight into the state of the company’s finances as well as the company’s current and future market position and sales potential. Whether you are planning to sell tomorrow or just trying to gauge where you stand compared to the competition, a business valuation service can give you an idea of your company’s worth. This blog aims to provide you with a complete guide to business valuation and equip you with the knowledge you need to apply it to your operations. So let’s kick off with an introduction.

Companies can have their worth estimated through a method called “business valuation” or “company valuation.” Throughout the valuation process, every aspect of a company and each of its subunits is evaluated to establish a dollar value.

Company valuations are performed for many purposes, including but not limited to determining a business’s fair market value in preparation for sale, determining who owns what shares of a business, settling tax disputes, and settling marital property disputes. In addition, many business owners consult with external business evaluators to objectively assess their company’s worth.

Understanding the business valuation basics

Valuation is a common topic of conversation in the world of corporate finance. If your company is considering the sale of all or part of its operations, a merger, or an acquisition, you will likely want get your business valued. However, when valuing a company, it’s important to consider all of the factors that contribute to the company’s current worth to arrive at an accurate estimate.

Considerations such as management, capital structure, future earnings potential, and market value of assets may all go into a business’s valuation. Valuation methods and techniques can range widely between professionals, companies, and sectors. For example, financial statement analysis, discounted cash flow models, and peer company comparisons are typical methods used to determine a firm’s worth.

Furthermore, accurate valuation is essential for tax purposes. For tax purposes, the IRS (Internal Revenue Service) mandates that a company’s worth be determined by its current fair market value. For example, a firm’s shares may be subject to capital gains or gift taxes upon sale, purchase, or transfer of ownership.

After the basics business valuation benefits must be understood to know why it’s critical in the present era to get it done.

Benefits of business valuation: Why should you get it done?

By considering a company’s workforce, assets, intellectual property, earnings, growth, and losses, an appraisal or valuation can accurately portray the company’s current economic value.

Every business owner, for whatever reason, should think about having their firm valued once a year. Being confident in the company’s real value will help the owner(s) make the right decision.

To understand better, let’s have a look at the following business valuation benefits:

Helps in knowing the performance of the business

The main advantage of conducting a business appraisal/valuation is that it aids in comprehending a business’s performance.

An analysis of a company’s financial records over the past five years is crucial to the business valuation process. The study is conducted from multiple perspectives for the business valuer to identify recurring trends and growth patterns.

Furthermore, the business valuer will analyze the company’s liquidity, coverage, leverage, and operational ratios during the last five years. They also create a complete, industry-specific analysis to assess the company’s financial health.

In this way, business owners can make impartial assessments of the company’s health and performance. It also gives them a comprehensive understanding of the company’s development, profitability, debt capacity, and liquidity.

Additionally, owners can better gauge the company’s real performance by comparing each of these metrics to the industry average.

This in-depth research acts as a valuable instrument for benchmarking purposes. It is so because it is through statistical analysis that a company’s management, investors, and other interested parties may identify and comprehend its unique growth patterns and financial health.

In addition to providing the CFO with some much-needed impartiality, this operational analysis may aid in managing a wide range of financial responsibilities. For example, company financial tasks may involve financial planning, risk assessment, capital allocation, financing analysis, and forecasting.

The CFO may then use this information to make sound strategic decisions that will help the firm thrive in the future, thanks to the insights gained from this analysis.

Know Your Business’s True Worth Today!

Whether you’re planning to sell, seeking investment, or analyzing your competition, our business valuation expertise will provide you with in-depth insights on market dynamics.

Business owners can be caught off guard by unsolicited offers to purchase their company. You may have a hazy idea of the company’s worth.

It’s likely that business owners rely on skewed market data, such as imprecise descriptions of the terms of deals. Without access to reliable market data and specifics about the sales at hand, this leads to an inflated valuation of the company.

A business owner’s untimely demise or incapacity is just one of many potential disruptions. Such an event could necessitate the exercise of a buy-sell agreement and the redemption or sale of some or all of the affected parties’ ownership stakes in the company. In addition, frequent business evaluations put a company in a better position to deal with such unexpected events. Better outcomes are achieved because expectations surrounding such events are better addressed.

Knowing the company’s worth can help prevent costly and contentious buy-sell agreement conflicts in private companies with various equity holders. A professional appraiser can greatly assist legal counsel in establishing the amount of value in a buy-sell deal. This allows for a fair valuation to be applied based on the circumstances surrounding the buy-sell agreement’s triggering event. The equity’s value can be expected to follow the pattern established by the annual valuation. Claims of bias become more likely when a single valuation is done after a triggering event occurs.

Helps in resolving disputes between partners

A disagreement between partners can arise due to multiple factors. Contractual disagreements, as well as purchase and shareholder disputes, are frequent dispute occurrences. Disputes involving contracts usually stem from one or both parties’ actions that violate the terms of the agreement, such as a broken promise to complete a project or provide promised services. However, mergers and acquisitions (M&A) and private equity (PE) investments are the root cause of acquisition and shareholder disputes.

There is a growing trend toward turning to third-party dispute resolution services like arbitration and mediation. Accurately valuing a corporation is a crucial first step in settling such disagreements. However, keep in mind that there are a wide range of factual circumstances that can lead to a dispute. Such events can include the end of a business collaboration or a disagreement over a failed merger.

As a result, whenever such disagreements arise, arbitrators are typically forced to choose between two conflicting expert analyses. First, there will be two expert reports, one prepared by each side of the dispute. In addition, each side of the argument produces its own value analysis based on the evidence it believes provides the strongest support for its position.

Therefore, it is critical to effectively communicate the conflict resolution findings by building a comprehensive and accurate valuation model. Finally, it encapsulates the essence of the requirement for an expert and the function they serve in conflict resolution or litigation.

Assists in estate tax planning

A company might prepare for potential estate taxes by having a valuation performed. Additionally, a business evaluation may aid in future tax planning, whether that involves preparation, mitigation, or payment.

The company’s estate must be liquid enough if it chooses to pay the estate taxes and makes no effort to avoid doing so. A business owner can ensure that his heirs do not have to sacrifice their standard of living or the company’s success because of tax obligations by engaging in careful tax planning.

A business’s estate taxes can be estimated and planned for with the help of a thorough valuation of the company. The business value may aid the owner and his advisors in formulating a strategy to minimize the estate.

Helps prepare for mergers and acquisitions (M&A)

Knowing that the asking price is fair is essential for any company looking to make an acquisition. To the same extent, a company looking to sell itself should know how much a rational buyer would be willing to pay. Additionally, if a company is thinking of merging with another, it needs to figure out how to divide up the ownership of the combined company fairly. In this case, the two companies’ value before the merger or acquisition is used to determine the ownership split.

Therefore, evaluating a company’s fair value is crucial to an M&A deal’s success, making business evaluation one of M&A’s most crucial components.

It’s important to remember that the negotiations and the post-M&A period are profoundly impacted by the accuracy and realism with which company values are determined. Research shows that many merger and acquisition (M&A) deals either fail or pay the target company more than they are worth. Inaccuracies in valuing businesses correctly lead to this situation.

Therefore, the combined companies cannot achieve their desired synergy after the M&A. The term “synergy” describes the enhanced value created by a merger between two companies.

It’s important to remember that business estimation isn’t just useful for owners who want to know how much their company is worth. Also, it aids them in maximizing profit in the event of a sale, merger, acquisition, JV, or strategic alliance.

A company’s value depends partly on its ability to generate profits and cash flow and partly on the time value of money. It is useful in calculating the price a company is willing to pay for another and the discount rate that should be applied to the future cash flows expected from the combined businesses.

In this section, we will discuss the main business valuation methods. But before we do that, let’s briefly understand why should you get your company valued.

The company may want to invite new investors, or one of the current shareholders may wish to cash out. In this scenario, a company valuation is required to establish the worth of the company’s shares.

Depending on the business’s needs, owners could pursue either equity or loan funding. In this instance, prospective financiers can assess the company’s worth before deciding whether or not to put money into it.

The owner may be considering selling their business. Knowing the company’s true worth maximizes the return on investment.

Coming back to the business evaluation methods, there are three most commonly used ones:

Asset-Based Approach

Market Value Approach

Earning Approach

We’ll now learn about each approach individually, starting with the asset-based approach.

Asset-based approach

Businesses are often valued based on their tangible assets, such as property, plant, and equipment. However, businesses also have intangible assets that can be just as valuable, if not more so. These include patents, copyrights, customer lists, and relationships with suppliers. The asset-based approach to valuation looks at a company’s tangible and intangible assets and assigns a value to each.

The total value of the company is then equal to the sum of all its assets. This approach is different from the traditional earnings-based approach in that it doesn’t focus on past or future profitability. Instead, it simply looks at what the company owns right now and tries to ascertain how much those assets are worth.

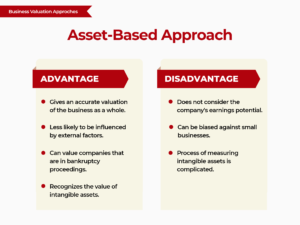

Advantage

There are many advantages to using the asset-based approach:

First, this method is often used when valuing businesses for sale, as it provides a more accurate estimate of the value of the company’s assets. The asset-based approach considers the company’s physical and intangible assets and assigns a value to each. This allows for a more precise valuation of the company as a whole.

Another advantage of this approach is that it is less likely to be influenced by outside factors such as the current economic climate. This can be especially helpful when valuing companies that are not currently profitable but have significant assets.

The asset-based approach can also be used to value companies that are in bankruptcy proceedings.

Further, it also recognizes the importance of intangible assets, such as goodwill and intellectual property. These types of assets are often overlooked when using other valuation methods, such as the market or the income approach. By taking them into account, the asset-based approach provides a complete picture of the company’s true value.

Disadvantage

There are several disadvantages to the asset-based approach:

This method does not account for the company’s earnings potential or future growth prospects. This can lead to an inaccurate valuation of the company.

The asset-based approach can be biased against small businesses since their total assets may be less than those of larger businesses. This can make it difficult to compare businesses of different sizes.

Since internally generated products don’t appear on the balance sheet, the process of measuring intangible assets can be quite complicated.

These assets can be difficult to value but can add significant value to a company.

How to value a business using the asset-based approach

The asset-based approach is one of the most commonly used methods for valuing a business. This approach values a business based on the fair market value of its assets. The key to this method is determining what the assets are worth if they were sold on the open market.

To value a business using the asset-based approach, you will need to:

Determine the fair market value of all of the company’s assets. This includes both physical assets (property, equipment, inventory) and intangible assets ( patents, copyrights, goodwill).

Subtract any liabilities from the total asset value. This will give you the net asset value of the company.

Adjust the net asset value for any special circumstances that may exist. For example, if there are significant liabilities that must be paid off before the assets can be sold, this should be taken into account.

Divide the adjusted net asset value by the number of shares outstanding to arrive at a per-share value for the business.

Two main or commonly used methods under the asset-based approach are:

Asset Accumulation Valuation

Excess Earnings Valuation

Asset Accumulation Valuation

Similarities between the well-known balance sheet and the asset accumulation strategy immediately appear at first glance. The asset accumulation approach adds a company’s assets and liabilities and gives values. The business value here is the difference between the asset value and the liability value of the company.

Though seemingly easy at first, the challenging part is in the details. Accurately listing all assets and liabilities is essential. Furthermore, the asset accumulation approach must have a reliable technique for assigning asset and liability values.

Some factors considered in valuation aren’t necessarily reflected in a normal set of financial statements. Some examples are intellectual property developed internally, such as patents and trade secrets. Provisional obligations are also included, such as those associated with meeting regulatory requirements or pending litigation.

Excess Earnings Valuation

The excess earnings method, on the other hand, combines elements of both the income and asset approaches to valuation. Goodwill can be calculated using the same procedure as the company’s tangible assets and liabilities.

To calculate goodwill, a company’s profits are viewed as an input, and a link is made to the income approach. As a result, the excess earnings approach is favored when solid enterprises with significant goodwill need to be valued.

Accounting firms, law offices, medical clinics, and architectural firms are all common examples of businesses benefitting from the excess earnings method. Valuing manufacturing businesses and mature IT companies is also included.

The market value approach is a business evaluation method that looks at the company as a whole and determines its value based on what similar businesses are worth. This approach is often used when valuing closely held companies or family-owned businesses.

To calculate the market value of a company, appraisers will look at comparable sales data for similar businesses. This data can be pulled from public records, private transactions, or brokerages specializing in business sales. Once this data is collected, it is analyzed to determine a range of possible values for the company being valued.

Advantage

When valuing a business, several different approaches can be taken. For example, the market value approach is one option that can be used and has many advantages.

One advantage of the market value approach is that it considers the current market conditions when valuing a business. This is important because businesses are constantly changing in value based on the current market conditions. You can get a more accurate business estimation using the market value approach.

Another advantage of the market value approach is that it is relatively easy to calculate. This makes it an attractive option for businesses that want to get a quick and easy valuation.

Disadvantage

While there are certain advantages to using the market value approach, there are also some drawbacks.

One drawback is that this method relies heavily on accurate data for comparable sales. If this data is unavailable or does not reflect current market conditions, then the valuation results may not be accurate.

Additionally, this approach does not take into account specific factors about the company being valued, which could impact its value (such as brand equity or unique products/services).

How is the market value approach used in business valuation?

The market value approach is used to estimate the worth of a company by looking at its recent sales price and earnings. This approach is based on the idea that a company is worth what someone is willing to pay for it.

To calculate the market value of a company, analysts will look at its recent sale prices and earnings. They will also look at comparable companies in the same industry to see what they are selling for. Based on this information, they will come up with a range of possible values for the company.

The market value approach is useful for valuing companies that are publicly traded. It can also be used for private companies, but it may be more difficult to find comparable companies to use in the analysis.

There are two main approaches to this method which we will discuss in brief:

Public Company Comparables Method

Precedent Transactions Method

Public Company Comparables Method

The Public Company Comparables Method is a valuation method that uses the market value of publicly traded companies to estimate the value of a privately held company. This method is sometimes called the market approach or the guideline company method.

To use this method, the appraiser will identify a group of comparable companies and then adjust those companies’ values to account for differences between the companies and the subject company. The appraiser will then use these adjusted values to calculate an estimated value for the subject company.

This method can be useful when there are no similar transactions to use in a valuation or when public market data is more readily available than private transaction data. However, this method can be less reliable than other methods because it is based on estimates and assumptions. In addition, this method may not be appropriate when there are few publicly traded companies in the same industry as the subject company or when the subject company is significantly different from its peers.

Precedent Transactions Method

The precedent transactions method is a valuation method that uses the prices of similar transactions to estimate the value of a business. The principle behind this method is that the market value of a business is determined by the prices paid for similar businesses.

This method can be used to value companies, businesses, and intangible assets such as patents and copyrights. It is commonly used in M&A transactions.

To use this method, the first step is to find comparable companies that have been sold in the past few years. This can be done by searching online databases or contacting brokerages specializing in business sales. Once you have a list of comparable companies, you will need to adjust their sale prices for factors such as size, growth potential, and profitability.

Once you have adjusted sale prices for these factors, you can estimate the company’s value using one of two methods: the mean value method or the median value method. In the mean value method, you simply take the average of all the adjusted sale prices. In the median value method, you take the middlemost sale price after sorting all the adjusted sale prices from highest to lowest.

The earning approach is a business valuation method that estimates the company’s value by looking at its past and projected earnings. This method is also sometimes referred to as the income approach.

There are two main types of earnings that can be used in the earning approach: historical earnings and projected earnings. Historical earnings are simply a record of a company’s past financial performance. Projected earnings are future-oriented and consider things like expected growth, changes in the marketplace, etc.

When valuing a business using the earning approach, two key components must be considered: the discount and capitalization rates.

The discount rate accounts for the time value of money and risk. In other words, it reflects how much someone would be willing to pay for a stream of future earnings that are not guaranteed. The higher the risk, the higher the discount rate will be.

The capitalization rate is used to convert projected or historical earnings into an estimate of business value. It essentially tells you how much someone would be willing to pay for each dollar of earnings. For example, if a company has projected earnings of $100,000 and a capitalization rate of 10%, then its estimated value would be $1 million ($100,000 x 10%).

Advantage

The earning approach is the most common method used to value a business. This approach values a business based on its ability to generate income.

The main advantage of using this approach is that it is easy to understand and calculate. This approach is also widely accepted by investors and lenders.

Another advantage of the earning approach is that it can be used to value businesses of all sizes. This makes it an ideal method for small businesses that may not have the same financial data as large businesses.

It is the most commonly used method for valuing a business. This is because it provides a quick and easy way to estimate the value of a company based on its ability to generate income.

Disadvantage

There are several potential disadvantages of using the earnings approach:

It can be challenging to accurately predict future earnings, particularly over the longer term. This can make this method less reliable than other valuation methods.

The earnings approach does not consider non-financial factors that may be important when valuing a business, such as its location, brand value, and customer base.

This method can be time-consuming and expensive to calculate, particularly if extensive financial data is not available.

Know Your Business’s True Worth Today!

Whether you’re planning to sell, seeking investment, or analyzing your competition, our business valuation expertise will provide you with in-depth insights on market dynamics.

How to Value a Business Using the Earning Approach?

The earning approach in company valuation is a method of estimating the economic value of a company by looking at its historical earnings. This approach is based on the premise that a company’s future earnings potential is directly related to its past performance.

To value a business using the earning approach, analysts typically begin by reviewing a company’s financial statements and calculating its average annual earnings over a period of time. They then adjust these earnings for inflation and any one-time or non-recurring items. Next, they estimate the company’s future earnings potential based on expected changes in sales, costs, and profits. Finally, they discount these future earnings back to present value using a reasonable rate of return.

The earning approach is commonly used in conjunction with other valuation methods, such as the market and asset-based approaches. These different methods can provide a more comprehensive picture of a company’s true worth when used together.

The following are the main approaches to this method which are worth discussing:

Capitalization of Earning Method

Discounted Cash Flow Method

Capitalization of Earnings Methods

The capitalization of earnings method is a valuation technique used in the income approach to estimate the value of a business, investment property, or natural resource. The method is based on the principle that the value of an asset is equal to the present value of its future net cash flows.

It is commonly used to value businesses and investment properties because it considers both the earning power of the asset and the risk associated with those earnings. The technique can be applied to any type of asset, but it is most often used to value companies that do not have a history of paying dividends.

To calculate the value using the capitalization of earnings method, you must first estimate the asset’s future net cash flows. This requires making assumptions about sales growth, operating expenses, and interest rates. Once you have estimated the future cash flows, you then discount them back to present value using a suitable discount rate. The resulting present value is your estimate of the asset’s value.

Discounted Cash Flow Approach

Discounted cash flow (DCF) is a valuation method that estimates the present value of future cash flows. DCF valuation is based on the time value of money, which states that a dollar today is worth more than a dollar in the future. The discount rate used in DCF valuation is the opportunity cost of capital, the minimum return an investor would require to invest in a company.

The key inputs in DCF valuation are:

– Cash flows: These are estimated future cash flows for the company being valued.

– Discount rate: This is the opportunity cost of capital.

– Terminal value: This is the company’s estimated value at the end of the forecast period.

DCF valuation can be performed using either the intrinsic value approach or the relative valuation approach. Intrinsic value DCF valuation estimates the present value of all future cash flows for a company. Relative value DCF valuation compares a company’s present value of cash flows to other companies in its industry.

The advantage of DCF valuation is that it considers all potential revenue sources and costs for a company over its lifetime. The disadvantage of DCF valuation is that it requires forecasts of future cash flows, which can be difficult to estimate accurately.

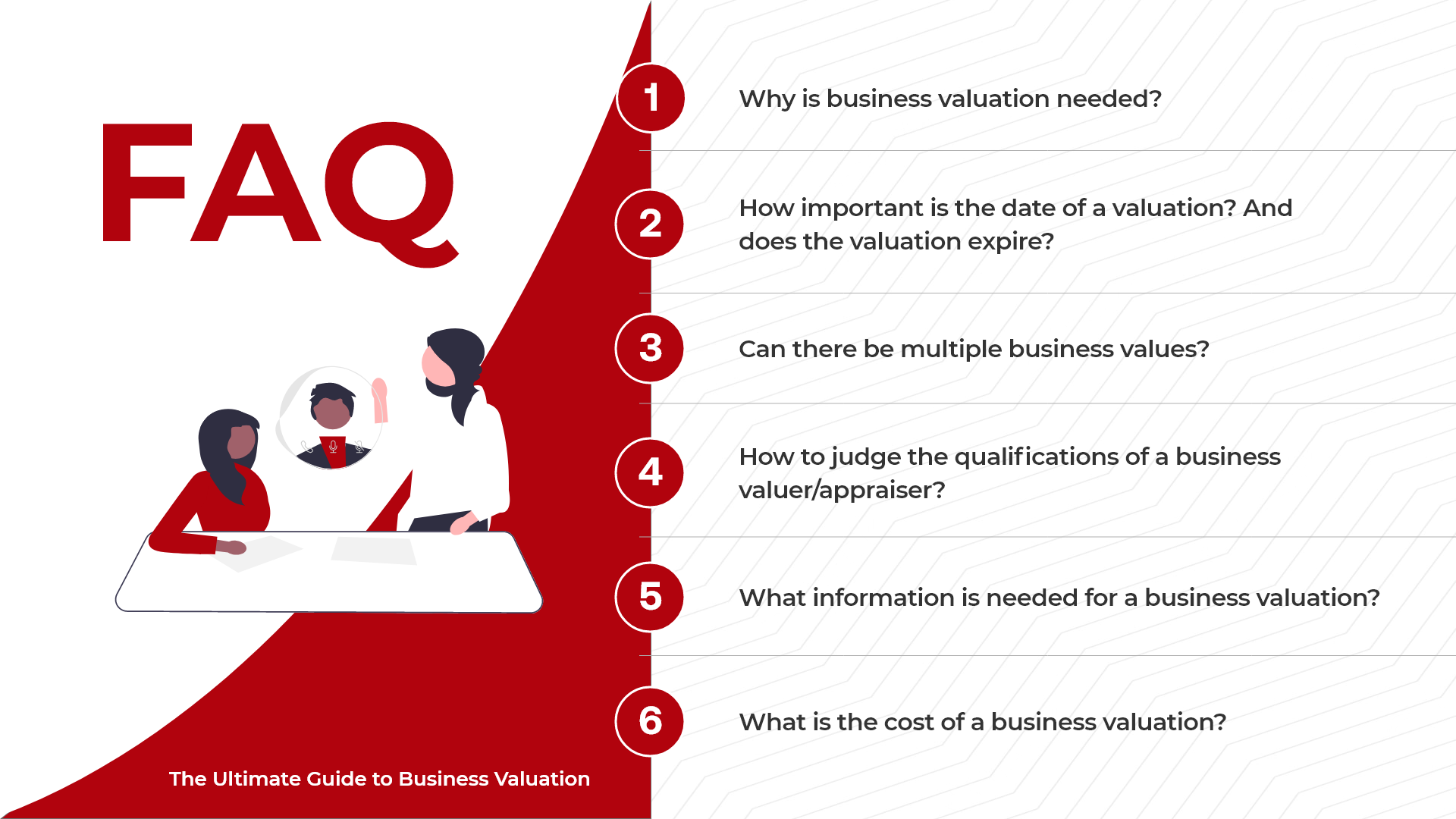

Frequently Asked Questions

Why is business valuation needed?

The reason behind getting a business valuation done comes under the following sorts:

Transaction: Planning to exit, financing, buy-sell deal, fairness opinions

Litigation: Fraud, bankruptcy, shareholder, and marital disputes

How important is the date of a valuation? And does the valuation expire?

An enterprise valuation is an opinion of the firm’s worth as of a particular date. Different internal and external factors might affect a company’s value at different times. However, the value generated from an out-of-date valuation report may no longer be relevant because a business estimation is always accurate as of the day it was conducted.

Can there be multiple business values?

Yes. The worth of a company might fluctuate over time and have more than one possible outcome. However, when estimating a company’s value, it’s essential to consider how much a willing and able buyer would pay. In this way, the company value can vary depending on whether it is being acquired by a strategic acquirer who can realize enhanced value or a willing buyer who receives no synergistic benefits.

How to judge the qualifications of a business valuer/appraiser?

Professional valuation is a field that encompasses a wide variety of experts. It is true that only trained and experienced certified business assessors can provide legally binding estimations of a company’s value. Earning either the Certified Business Appraiser (CBA) or Accredited Senior Appraiser (ASA) accreditation is a significant accomplishment in business valuation appraisal. So, these professionals require tremendous training and expertise compared to those with Accredited in Business Valuation (ABV) and Certified Valuation Analyst (CVA) certifications.

What information is needed for a business valuation?

The following is the list of documents necessary to have a precise valuation:

Interim P&L statements and the current year balance sheets

P&L statements, balance sheets, and tax returns of the past five years

Copies of any projections or forecasts

Other documents are commonly required, like information expressing the company’s service and/or products, liability details, a list of important assets, and reports by other professionals, if any.

What is the cost of business valuation?

Most qualified company appraisers will provide a price based on a flat charge, per-hour rate, or a percentage of the total amount to be appraised. The cost can be anywhere from $5,000 to over $50,000, though this varies widely depending on factors like company size, industry, and the nature of the valuation’s intended use.

Conclusion

This was an in-depth business valuation guide that included a brief introduction, the benefits of getting company valuation, the different valuation methods, and a “Frequently Asked Questions” section. It gives you all the details you need to have your company valued and the importance of it.

Now, if you are an owner looking for business appraisal services from a business valuation expert, Arrowfish Consulting can be your go-to solution for it. Having a combined experience of over 100 years, our business appraisal team is considered a valuation industry expert by all our clients. Our company has “qualified appraisers” who are familiar with the rules and regulations the Internal Revenue Service (IRS) set forth for gift and estate appraisals. Further, our team includes ASAs, CVAs, CPAs, CFAs, financial analysts, and economists that provide various company appraisal services.

Hop on a call with our client support team and book a free consultation with one of our experts to help understand your problem or needs and provide the best possible solution.

Jeremiah Grant is the Managing Partner of Arrowfish Consulting. In addition to acting as a primary liaison for many of the firm’s engagements, He primarily focuses on business valuation and economic damages expert witness assignments, in addition to forensic accounting and insurance claims analysis.

Learn the essential methods and factors for pharmacy valuation. Understand SDE, EBITDA, and more. Get expert help for a precise appraisal. Contact us today!

Discover how to value a private equity firm with proven techniques like DCF, CCA, and market comparables. Get accurate insights for better investment decisions!

Learn how to value a luxury goods business with proven methods, key financial metrics, and market trends. Get expert insights to make informed decisions today!

Learn how to value a health and wellness business using key methods and financial metrics. Get expert insights to maximize your business’s worth—start now!

Learn how to value a sports franchise using revenue, market size, and financial metrics. Explore key valuation methods and insights. Read our full guide now!